Online Payment Platforms: Key Features & Top 12 Solutions in 2026

What Is an Online Payment Platform?

Online payment platforms like Luqra, PayPal, and Stripe allow businesses to accept payments online, as well as digital wallets like Apple Pay and Google Pay, which allow customers to pay conveniently. These platforms work as a secure intermediary between the customer, merchant, and bank to process credit cards and other payment types.

Online payment platforms began gaining traction in the late 1990s and early 2000s as e-commerce emerged. PayPal, founded in 1998, was one of the first widely adopted systems, initially used for payments on eBay. Its success demonstrated the demand for secure, user-friendly digital transactions.

In the 2010s, the landscape expanded with the rise of mobile-first platforms like Square and digital wallets like Apple Pay and Google Pay. These innovations reflected the growing importance of smartphones in commerce and enabled more flexible, contactless payments.

The 2020s have seen the rapid scaling of global platforms that emphasize developer-friendly APIs and seamless integration with web apps. As digital commerce becomes standard across industries, online payment tools have become more specialized, with solutions tailored for subscription billing, marketplaces, and international transfers.

This is part of a series of articles about payment methods.

In this article:

Modern online payment platforms are built with several integrated components that ensure secure, reliable, and efficient transactions. These components handle everything from transaction initiation to settlement, fraud prevention, and compliance.

Payment gateway: Acts as the interface between a merchant’s website and the financial network, securely capturing and transmitting payment details for authorization.

Payment processor: Communicates with card networks and banks to execute the transaction, moving funds between the buyer’s and seller’s accounts.

Merchant account: A type of bank account where funds from customer payments are temporarily held before being transferred to the business’s primary account.

Tokenization service: Converts sensitive payment data into non-sensitive tokens, reducing the risk of data breaches and simplifying PCI compliance.

Fraud detection and risk management tools: Use algorithms and machine learning to detect suspicious activity, block fraudulent transactions, and reduce chargebacks.

PCI compliance layer: Ensures the platform adheres to Payment Card Industry Data Security Standards (PCI DSS), protecting cardholder data during and after transactions.

APIs and SDKs: Enable developers to integrate payment functionality into websites, mobile apps, or other platforms with minimal effort.

Reporting and reconciliation tools: Provide merchants with dashboards and reports to monitor transactions, manage payouts, and reconcile payments with accounting systems.

Dispute and chargeback management: Helps merchants respond to transaction disputes by supplying evidence and managing chargeback workflows.

Currency conversion and cross-border support: Enables international payments by handling currency exchange and local compliance in different regions.

Here is the general process followed by most online payment platforms:

- When a customer initiates a transaction, the online payment platform begins by collecting payment information through a secure interface, typically via a web form, mobile app, or point-of-sale (POS) system. This data is immediately encrypted and sent to the payment gateway.

- The payment gateway routes the information to the payment processor, which contacts the customer’s issuing bank through the card network (e.g., Visa or Mastercard) to request authorization.

- The issuing bank checks the account for sufficient funds or credit, performs fraud checks, and then either approves or declines the transaction.

- If approved, the authorization is sent back through the processor and gateway to the merchant. The transaction is then captured, and funds are reserved. Settlement happens later, typically within one to two business days, when the funds move from the customer’s bank to the merchant’s account via the acquiring bank.

Throughout this process, tokenization and encryption protect sensitive information. Simultaneously, fraud detection tools analyze the transaction in real time, looking for unusual patterns or anomalies. If flagged, the transaction may be paused or blocked.

The platform also generates reports and logs for tracking, reconciliation, and dispute resolution. If a customer later contests the charge, the platform initiates the chargeback process, helping the merchant respond with supporting documentation.

1. Luqra

Luqra is a merchant and client-first payment platform that helps businesses through the power of Luqra’s top-tier support and infrastructure. From small merchants to large and scaling businesses, Luqra offers seamless payment services that manage transactions, chargebacks, fraud, VAMP monitoring, and security, all while supporting scaling and growth. It prioritizes fraud prevention and protection, lower fees and reserves, minimal account freezes, and 24/7 customer support that strengthens merchants in a wide range of industries from dropshipping and e-commerce to telehealth and biotech.

Key features include:

- Hundreds of Direct Integrations: A system and UI that works with many of the platforms merchants use, like Shopify, NMI, Salesforce, and many more

- Competitive pricing: Pricing customized to help you scale, not limit your revenue, with the uncapped merchant accounts that modern businesses demand

- 24/7 in-house customer support: US-based customer support available 24/7, all year round

- Dedicated reps: Customer support that actually knows business details because they’re the specific team member assigned to it

- Optimized fraud detection: Modernized fraud detection systems and tools that prioritize security and privacy

- Fast deposits and lower reserves: Faster deposits and limited reserves that deliver revenue instead of hoarding it

Source: Luqra

2. Stripe

Stripe is a unified online payment platform to help businesses accept payments and expand globally with minimal technical overhead. It offers a flexible infrastructure that supports a range of payment methods across online, mobile, and in-person channels. It has built-in tools for fraud prevention, localized payment optimization, and automated compliance.

Key features include:

- Optimized checkout suite: Prebuilt UI components and one-click checkout improve conversion and reduce engineering effort

- Global coverage: Accept payments in 195 countries and 135 currencies with extensive local acquiring support

- 100+ payment methods: Provides popular options like cards, bank debits, buy now/pay later, and regional wallets

- AI-powered fraud prevention: Stripe Radar detects and blocks fraud using data from billions of transactions

- Fraud prevention: Stripe Radar uses AI and billions of data points to detect and prevent fraud in real time

Source: Stripe

3. Square

Square is a flexible payment platform that enables businesses to accept payments anywhere, online, in person, or remotely, with minimal setup and no long-term contracts. Square provides a suite of tools for secure payment processing, cash flow management, and sales tracking. It supports a variety of devices and channels.

Key features include:

- Omnichannel payment support: Accept payments in person with Square hardware, online via Square Websites or APIs, and remotely through invoices or virtual terminals

- No contracts or hidden fees: Transparent pricing with no long-term commitments or surprise charges

- Fast access to funds: Next-business-day transfers for free and instant fund transfers for a small fee

- Offline payment capability: Continue accepting payments even without internet access, Square stores and syncs transactions once back online

- Built-in fraud protection and compliance: Includes PCI compliance, dispute resolution tools, and security features by default

Source: Square

4. Adyen

Adyen is an enterprise-grade online payment platform that allows organizations to manage payments at scale. It provides a single integration that supports a range of payment methods, devices, and markets.

Key features include:

- Unified global payments: Accept credit cards, digital wallets, and local payment methods across web, mobile apps, and recurring billing

- Multiple integration options: Drop-in, Components, or API-only

- Local payment method access: Support popular regional payment methods through one integration

- Revenue optimization: Boost conversion and authorization rates using machine learning models trained on real-time data

- Seamless authentication: Implement delegated authentication to balance security and checkout ease

Source: Adyen

5. PayU

PayU is an online payment platform that acts as both a payment gateway and processor. It manages the payment flow, from authorization to settlement, while optimizing for speed, security, and conversion.

Key features include:

- End-to-end payment flow management: Handles every stage of the transaction, including authorization, settlement, and routing across issuers and acquirers

- Dual role as gateway and processor: Simplifies integration and reduces technical overhead by managing both data transmission and transaction execution

- Global and local reach: Supports cross-border transactions with access to local acquirers and alternative payment methods

- Fraud prevention and risk controls: Uses algorithms and configurable fraud filters to prevent chargebacks and minimize revenue loss

- Instant retry feature: Automatically re-attempts failed transactions with alternate acquirers in real time to recover false declines

Source: PayU

{kind=link}

6. Maverick Payments

Maverick Payments is an online payment platform for businesses, ISOs, ISVs, and financial institutions seeking flexible and scalable payment solutions. It offers an infrastructure for online and in-person payments, with an emphasis on developer support, customization, and regulatory compliance.

Key features include:

- Online and in-person payments: Accept card, ACH, and digital wallet payments through websites, mobile devices, text, or point-of-sale terminals

- White-label platform: ISOs and financial institutions can offer branded payment solutions with no liability or backend infrastructure management

- Developer-centric tools: Real-time reporting, chargeback handling, and integration APIs tailored for ISVs and developers

- Custom solutions for specialty markets: Designed to support unique use cases and regulated industries with built-in fraud prevention and compliance

- Portfolio management and onboarding: Features include digital onboarding, multi-bank routing, and detailed portfolio insights through a unified dashboard

Source: Maverick Payments

{kind=link}

7. Clover

Clover POS is a cloud-based point-of-sale system to help businesses manage payments, inventory, staff, and customer engagement from a single platform. Suitable for retail, hospitality, and service-based businesses, Clover combines customizable hardware and software with analytics and a large app ecosystem to simplify operations.

Key features include:

- Flexible payment acceptance: Supports tap, swipe, dip, mobile wallets, contactless, and even check scanning

- Cloud-based real-time reporting: Track sales, refunds, and performance with customizable reports accessible from anywhere

- Customizable POS setup: Choose from a range of devices and apps to match business needs, from countertop systems to mobile units

- Built-in CRM tools: Manage customer profiles, order history, feedback, and loyalty programs from the same dashboard

- Employee and order management: Set roles, track sales performance, manage shifts, and simplify complex orders like splits and tabs

Source: Clover

{kind=link}

8. PayPal

PayPal is a global online payment platform that enables users to make purchases, send money, and receive payments using a secure digital wallet. It acts as an intermediary between customers and merchants, masking sensitive financial information and providing buyer protection. PayPal supports both personal and business transactions and is accepted by millions of online retailers worldwide.

Key features include:

- Secure payments: Protects customer card and bank details using encryption and tokenization during transactions

- Buyer protection: Offers reimbursement for eligible purchases if an item doesn’t arrive or doesn’t match the seller’s description

- Fast transfers: Allows instant or same-day money transfers to other users or to a linked bank account (fees may apply)

- Multi-currency support: Enables international transactions and holds balances in multiple currencies with built-in currency conversion

- Integrated checkout: Simplifies checkout with one-click PayPal login on partner websites and mobile apps

Source: PayPal

{kind=link}

9. Apple Pay

Apple Pay is a mobile wallet service for Apple devices, allowing users to make contactless payments in stores, in apps, and on websites. It uses tokenization and biometric authentication to enhance payment security and convenience. Card details are never shared with merchants or stored on Apple servers, making it one of the more secure payment methods available.

Key features include:

- Device-based authentication: Uses Face ID, Touch ID, or a passcode to authorize transactions securely

- Tokenized card numbers: Replaces real card data with a device-specific token to prevent exposure of sensitive information

- Broad acceptance: Supported by major retailers, e-commerce platforms, and transit systems in many countries

- In-app and web payments: Allows frictionless payments inside iOS apps and Safari browser without re-entering card details

- Private transactions: Apple does not track or store users' payment activity, maintaining user privacy

Source: Apple

{kind=link}

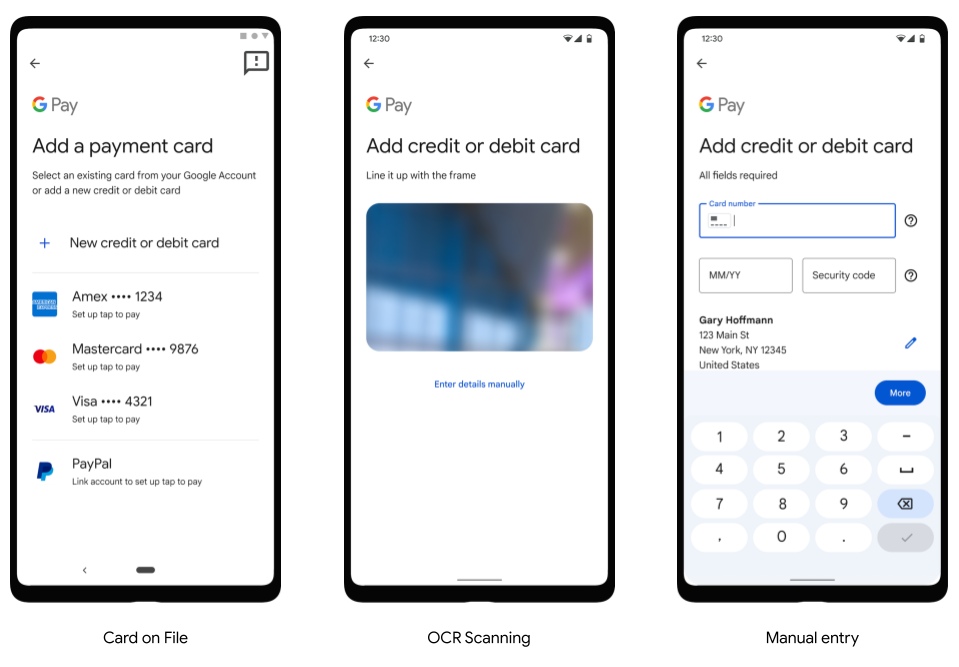

10. Google Pay

Google Pay is a digital payment service that works across Android devices and the web. It allows users to store debit cards, credit cards, loyalty programs, and transit passes, and pay seamlessly online or in physical stores. Google Pay uses tokenization and device-level security to protect transaction data, while offering a consistent checkout experience across supported platforms.

Key features include:

- Contactless payments: Use NFC-enabled Android devices to tap and pay at supported retail locations

- Autofill integration: Automatically fills in payment and shipping details on Chrome and Android apps for faster checkouts

- Secure by design: Transactions are encrypted and authenticated using PIN, fingerprint, or screen lock

- Unified wallet functionality: Stores not only payment methods but also gift cards, transit passes, and event tickets

- Cross-platform support: Works across Android phones, Wear OS devices, Chrome browser, and third-party apps

Source: Google Pay

{kind=link}

11. Venmo

Venmo is a peer-to-peer mobile payment platform for quick money transfers between individuals. It combines payment functionality with social networking features, allowing users to share notes or emojis with each transaction. Venmo also supports in-app purchases at partner merchants and offers a branded debit card for physical payments.

Key features include:

- Instant peer payments: Send or request money instantly using phone numbers, email addresses, or usernames

- Social feed: Share payment descriptions publicly or privately, making transactions more interactive and casual

- Merchant support: Accepted by select online and mobile businesses through the Pay with Venmo feature

- Venmo debit card: Lets users spend their balance directly and withdraw cash at ATMs

- Transfer options: Offers both free standard bank transfers and instant transfer options for a small fee

Source: Venmo

{kind=link}

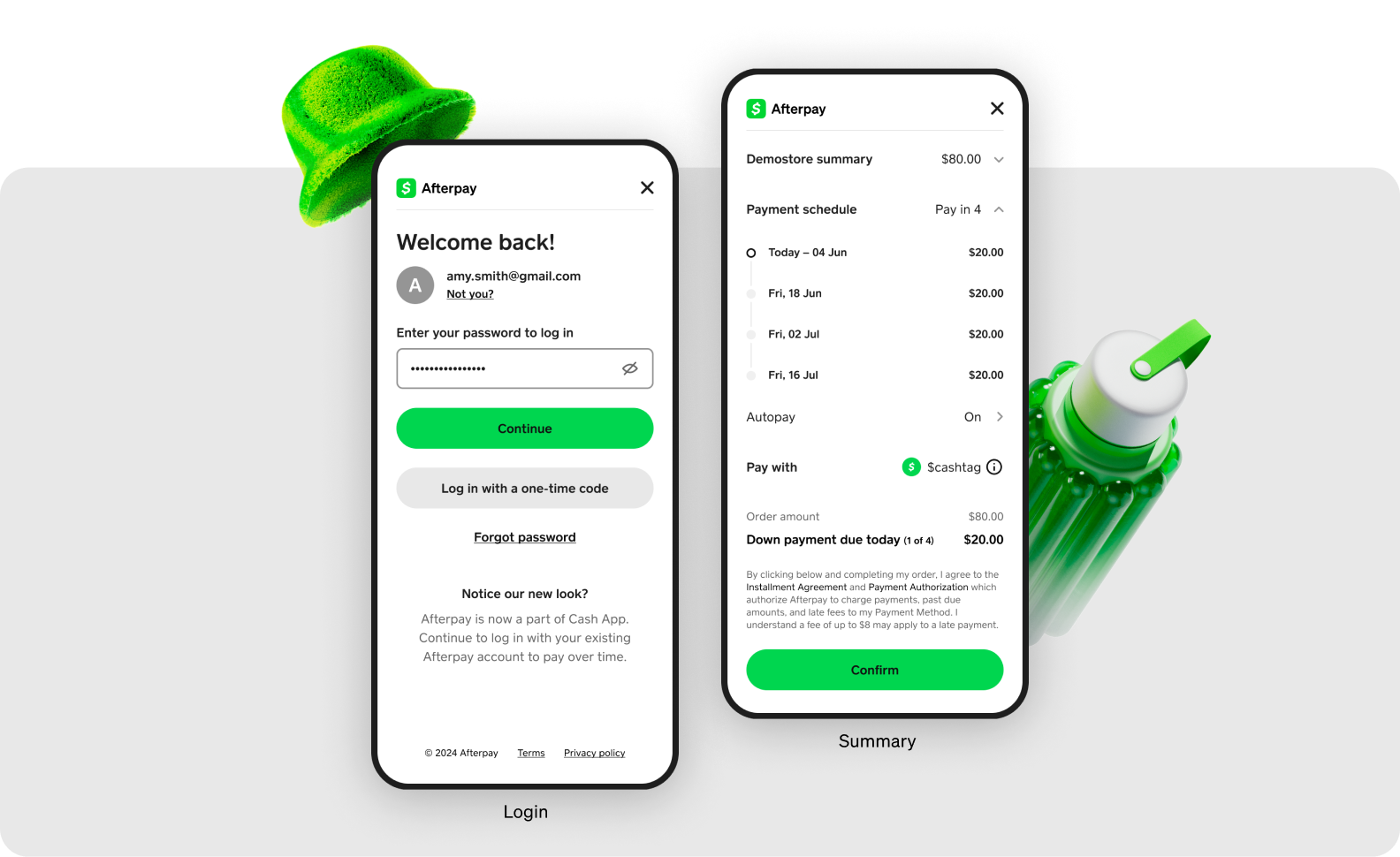

12. Cash App

Cash App is a digital wallet that combines money transfers, banking features, and investing capabilities in a single mobile app. It supports peer-to-peer payments, direct deposits, bitcoin transactions, and stock investing, making it a versatile tool for financial management. Users can also get a customizable Cash Card for in-store purchases and ATM access.

Key features include:

- Flexible money transfers: Send and receive payments instantly using unique $Cashtags or contact info

- Cash Card integration: Physical Visa debit card tied to the user’s balance, customizable and usable anywhere Visa is accepted

- Investment tools: Buy and sell stocks or bitcoin directly in the app, with no minimum balance required

- Banking features: Set up direct deposits for paychecks, tax refunds, or government benefits directly into Cash App

- Privacy and security: Offers PIN and biometric authentication, plus the ability to disable the card or payments remotely

Source: Cash App

{kind=link}

Selecting the right online payment processor is critical for ensuring smooth transactions, minimizing costs, and supporting business growth. The right choice depends on your business model, technical capabilities, customer base, and regulatory needs. Below are key considerations to guide your decision:

- Business type and volume: High-volume businesses may benefit from dedicated merchant accounts and subscription-based pricing. Small businesses or startups may prefer aggregators like PayPal or Square for easy setup and lower barriers to entry.

- Technical resources: Developer teams can leverage API-based platforms for custom workflows and integration flexibility. Businesses without technical teams might prioritize no-code or low-code platforms with ready-to-use checkout solutions.

- Geographic reach: If your customers are local, domestic processors offer faster settlements and better support for local payment methods. For international sales, choose a processor with strong cross-border capabilities, multi-currency support, and compliance with regional regulations.

- Accepted payment methods: Ensure the processor supports the payment types your customers prefer, including cards, wallets, bank debits, or buy now, pay later options.

- Cost structure: Compare transaction fees, monthly charges, and hidden costs. Understand how pricing models (flat-rate vs. interchange plus) affect your margins.

- Security and compliance: Look for built-in fraud prevention, PCI DSS compliance, tokenization, and tools for managing disputes and chargebacks.

- Integration and ecosystem: Consider whether the processor integrates with your existing tools, such as e-commerce platforms, accounting software, or CRM systems.

- Customer experience: Fast, seamless checkouts reduce cart abandonment. Evaluate the user experience, mobile optimization, and localization features.

- Support and reliability: Check for availability of customer support, service level agreements (SLAs), and redundancy measures to avoid downtime.

Conclusion

Online businesses need a scalable payment processing solution that supports growth without unnecessary holds, freezes, or volume caps. Luqra provides uncapped merchant accounts backed by extensive underwriting, helping ecommerce, subscription, digital goods, and high-volume online merchants operate with greater stability.

Direct integrations with Shopify, WooCommerce, Go High Level, Authorize.net, NMI, and SwipeSimple allow for seamless setup without downtime. Built-in fraud prevention tools, advanced chargeback management with Disputifier integration, and a proprietary VAMP monitoring dashboard help merchants stay compliant while reducing disputes. The centralized ERP system streamlines ticketing, chargeback responses, deposits, and transaction tracking in one place.

Merchants benefit from uncapped merchant accounts that support high-volume ecommerce growth, allowing businesses to scale without artificial processing ceilings. Disputifier-backed dispute automation reduces chargebacks, while real-time VAMP monitoring supports ongoing card network compliance. Seamless Shopify and WooCommerce integrations make implementation straightforward, and 24/7 in-house ecommerce risk support ensures merchants have access to knowledgeable assistance whenever it is needed.

For businesses seeking reliable online payment processing with long-term scalability, Luqra delivers a stable infrastructure designed to support consistent revenue growth.